What is Federal Excise Tax (FET) on Private Charter Flights?

From the NBAA Federal Tax Guide: All business aircraft operators, private and commercial, are required to pay Federal Excise Tax (FET) on the transportation of persons or property by air.

Federal Excise Tax can be determined as a percentage tax on the amounts paid for air transportation, a fuel tax, or a combination of the two. Charter flights, whether they are being operated under Federal Aviation Regulation (FAR) Part 135, private operation under FAR Part 125, or by airline operations under FAR Part 121, are generally subject to FET on air transportation and fuel.

Related: Understanding the Federal Aviation Regulations

Non-commercial aircraft operations (FAR Part 91) are generally only subject to FET on fuel. Still, some Part 91 flights can be subject to FET on air transportation.

For a complete guide on federal air transportation taxes, visit the NBAA website.

Does My Trip Require FET?

The only time FET is required is when your air transportation (i) both begins and ends in the United States or the “225-mile zone” (as defined below) and (ii) is directly or indirectly between two points in the United States, but only if the portion is not a part of uninterrupted international air transportation.

If the passenger makes payment for the trip outside of the United States, FET on air transportation will only apply to that portion of the trip that begins and ends in the United States.

FET on air transportation of persons applies to a flight that begins or ends in the 225-mile zone. The 225-mile zone is that portion of Canada and Mexico that is not more than 225 miles from the nearest point in the continental United States.

Locations not in Canada or Mexico, such as Nassau, Bahamas, are not part of the 225-mile zone. The 225-mile zone can be visualized as an area that is 225 miles above the United States order in Canada or 225 miles below the United States border in Mexico. For example, Vancouver and Toronto, Canada and Monterrey, Mexico are in the 225-mile zone. However, Edmonton, Canada and Mexico City, Mexico are not in the 225-mile zone.

Cities in Canada within the 225 Mile Zone

Baie Comeau, Quebec

• Brandon, Manitoba

• Calgary, Alberta

• Castlegar, British Columbia

• Charlottetown, PEI

• Comox, British Columbia

• Cranbrook, British Columbia

• Earlton, Ontario

• Forestville, Quebec

• Fredericton, New Brunswick

• Gaspe, Quebec

• Halifax, Nova Scotia

• Hamilton, Ontario

• Lamloops, Br. Columbia

• Kapuskasing, Ontario

• Kelowna, Br. Columbia

• Kenora, Ontario

• Lac du Bonnet, Manitoba

• Lethbridge, Alberta

• Little Grand Rapids, Manitoba

• London, Ontario

• Matane, Quebec

• Medicine Hat, Alberta

• Moncton, New Brunswick

• Mont Joli, Quebec

• Montreal, Quebec

• New Glasgow, Nova Scotia

• North Bay, Ontario

• Ottawa, Ontario

• Manitoba Penticton, Br. Col

• Port Hardy, Br. Col.

• Powell River, Br. Col.

• Quebec, Quebec

• Red Lake, Ontario

• Regina, Saskatchewan

• Rimouski, Quebec

• Saguenay, Quebec

• St. John, New Brunswick

• Saskatoon, Saskatchewan

• Sault Ste. Marie, Ontario

• Sept Isles, Quebec

• Sioux Lookout, Ontario

• Sudbury, Ontario

Cities in Mexico within the 225 Mile Zone

• Canarea, Sonora

• Chihuahua, Chihuahua

• Ciudad Jauarez, Chihuahua

• Ciudad Victoria, Tamaulipas

• Ensenada, Baja California

• Hermosilo, Sonora

• Matamoros, Coahuila

• Mexicali, Baja California

• Moncolova, Coahuila (Monterrey)

• Monterrey, Nuevo Leon

• Nogales, Sonora

• Nuevo Casas Grandes, Chihuahua

• Nuevo Laredo, Tamaulipas

• Piedras Negras, Coahuila

• Peynosa, Tamaulipas

• Tijiuana, Baja California

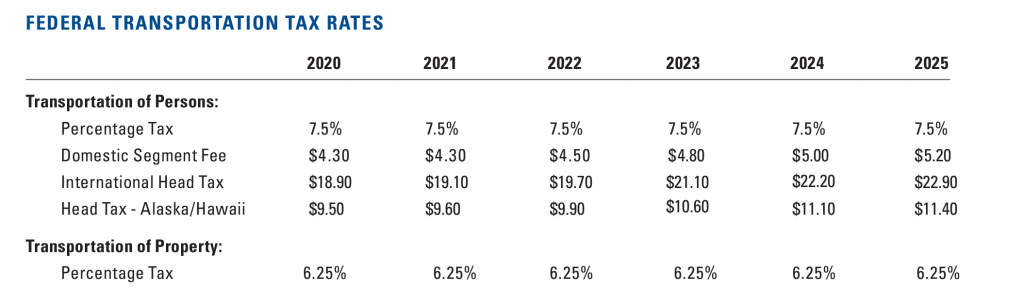

New Taxes for 2025

For 2025, the Percentage Tax for transportation of passengers and cargo remains the same at 7.5% and 6.25% respectively, however, the Domestic Segment Fee has increased from $5.00 to $5.20; the International Head Tax is up to $22.90 from $22.20; and the Head Tax for Alaska/Hawaii has been raised from $11.10 to $11.40.

Private Jet Charter Rates and Taxes

Although these are nominal increases, we like to keep our clients informed regarding changes in the private aviation industry. These taxes are included in every quote we provide, and you can learn more about private jet charter quotes here.

If you have any other questions about private jet charter rates and the applicable federal taxes, contact us or give us a call at 1-888-987-5387 and our brokers will be happy to discuss any questions you may have to provide you with the most transparent charter experience possible.

Air Charter Advisors is not a tax authority, or an aviation accounting firm. The information above is how we have interpreted the new FET rules set forth by the IRS. If you are an aircraft operator or an owner, please contact your accounting team. If you need a referral to an aviation accounting company, please contact us